Last updated: May 2026. Reflects the Skills in Demand framework that took effect on 7 December 2024 and the Annual Market Salary Rate amendments commenced on 25 March 2026. Always verify the latest figures with the Department of Home Affairs and Federal Register of Legislation before lodging.

Is Super Included in 482 Visa Salary? CSIT, SSIT and FWHIT Explained

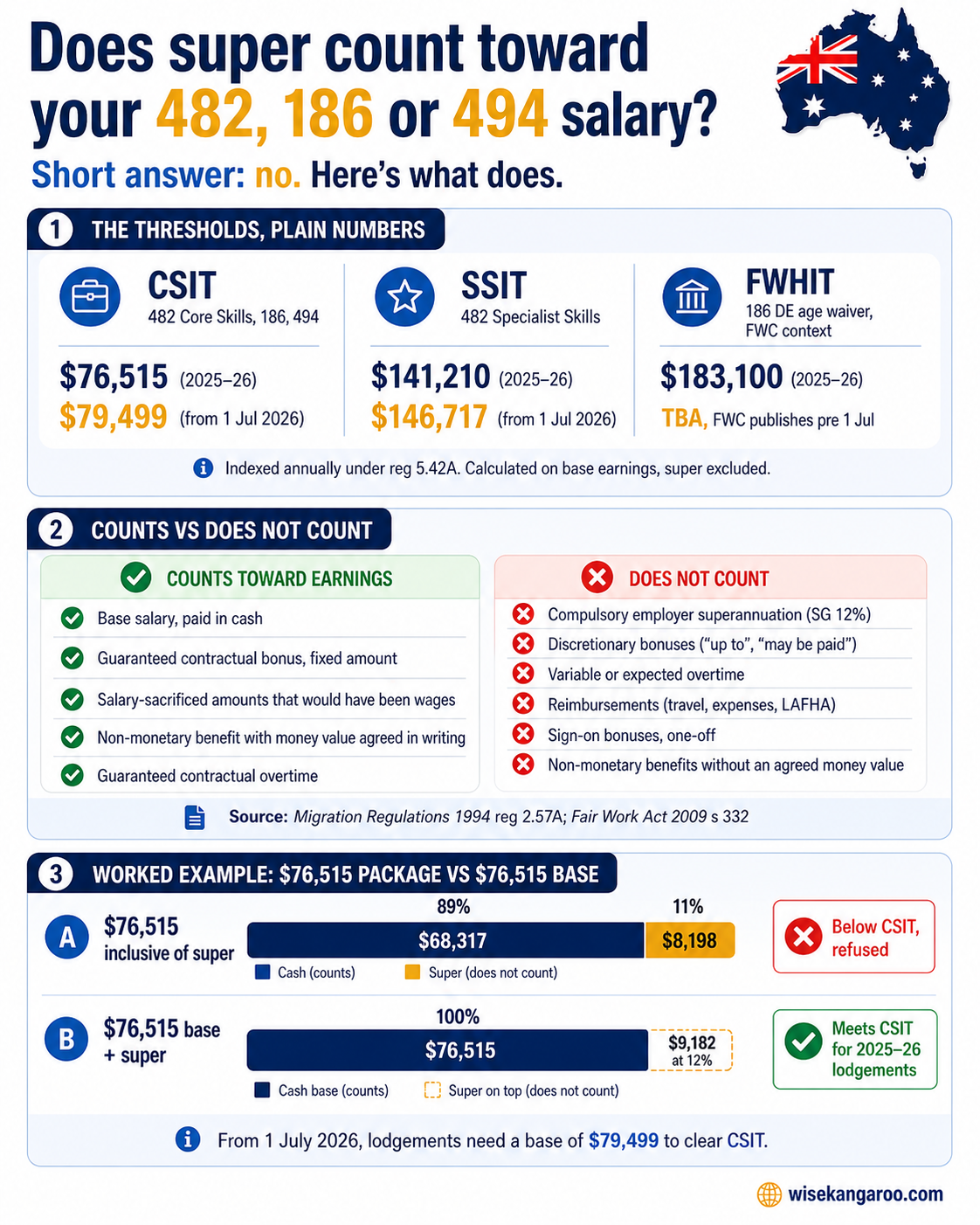

Short answer: no. Compulsory employer superannuation does not count toward the 482 visa salary threshold, the 186 nomination threshold, or the 494 nomination threshold. The relevant figure is base earnings, paid in cash, before super is applied on top.

That one rule trips up more nominations than almost anything else. An employer sees a $76,515 total package on a Core Skills nomination and assumes the threshold is met. Home Affairs looks at the same offer, removes the 12% superannuation guarantee component, sees the cash salary land below the current Core Skills Income Threshold, and refuses the nomination. The package looked compliant. The earnings figure was not.

This guide explains how “earnings” is defined for every income threshold that matters in employer-sponsored migration, including TSMIT (now retired), CSIT, SSIT, FWHIT and the Annual Market Salary Rate. We walk through a worked example for a 186 Direct Entry nomination at the threshold boundary and give you a checklist your finance team can run before signing the contract. If you also need to think about test scores in the same package, our explainer on the latest 482 English language requirements is the right companion read.

The thresholds in plain English

Since the Skills in Demand reforms commenced on 7 December 2024, the old TSMIT has been split into two operative thresholds. A third sits in the Fair Work system and shows up in employer-sponsored migration through age waivers and the Specialist Skills stream.

| Threshold | What it applies to | 2025 to 2026 | From 1 July 2026 |

|---|---|---|---|

| Core Skills Income Threshold (CSIT / TSMIT) | Subclass 482 Core Skills, Subclass 186 (all streams), Subclass 494 | $76,515 | $79,423 (confirmed under reg 5.42A) |

| Specialist Skills Income Threshold (SSIT) | Subclass 482 Specialist Skills | $141,210 | Indexation pending confirmation (projected ≈ $146,717) |

| Fair Work High Income Threshold (FWHIT) | 186 DE age waiver, 482 age and English concessions | $183,100 | $190,100 (published by Fair Work Commission, effective 1 July 2026) |

Indexation is automatic under reg 5.42A of the Migration Regulations 1994, driven by the November Average Weekly Ordinary Time Earnings release from the Australian Bureau of Statistics. No new legislative instrument is required each year.

The TSMIT acronym still appears across migration commentary and search results, but as of 7 December 2024 the operative thresholds are the CSIT and SSIT, set by LIN 24/094 and LIN 24/097. When a contract refers to “TSMIT”, read it as the CSIT for any role outside the Specialist Skills stream. Our TSMIT to CSIT primer covers the rename in more detail if it helps to anchor the language change for an internal audience.

Why super is excluded: the rule behind the rule

The legislative source is reg 2.57A of the Migration Regulations 1994, which sets out what counts as “earnings” for the sponsorship framework. Reg 2.57A is closely modelled on section 332 of the Fair Work Act 2009. Both provisions take the same approach.

Earnings include:

- Wages and salary

- Amounts applied or dealt with on the employee’s behalf, or as the employee directs (for example, salary-sacrificed amounts that would otherwise have been wages)

- The agreed money value of non-monetary benefits, where employer and employee have agreed a reasonable value in writing

- Guaranteed amounts that can be determined in advance

Earnings exclude:

- Compulsory employer superannuation contributions, to the extent the employer would otherwise have been liable for the Superannuation Guarantee charge

- Reimbursements

- Payments at the employer’s discretion

- Commissions, incentive payments and bonuses, unless the amount is contractually guaranteed and quantifiable in advance

- Variable overtime that is not a fixed contractual entitlement

The Superannuation Guarantee is a charge calculated on top of ordinary time earnings, not part of them. From 1 July 2025 the SG rate is 12%. That is real money to the employee, but it is not earnings under reg 2.57A or section 332, and it cannot be added to a base salary to clear a CSIT, SSIT, FWHIT or AMSR test.

Voluntary employer super contributions, paid above the SG amount, are different. Those amounts can count as earnings under section 332(4), and there is some Fair Work Commission case law treating them as part of the employee’s earnings rather than as compulsory super. If a contract includes voluntary employer super, get specific advice before relying on it for a threshold test.

The CSIT and SSIT are floors, the AMSR is the second test

A nomination has to clear two hurdles, not one. Both are calculated on the same earnings definition.

Hurdle one is the income threshold. CSIT for the 482 Core Skills stream, the 186 ENS streams and the 494. SSIT for the 482 Specialist Skills stream. The threshold is the legislated minimum; it is not a market test.

Hurdle two is the Annual Market Salary Rate. The nominator must show that the nominated annual earnings are at least the AMSR for the same occupation, in the same location, paid to an equivalent Australian worker. AMSR is set under reg 2.72 for the 482, reg 2.72C for the 494, and the equivalent ENS provisions for the 186.

The nominee is paid the higher of the two. If the AMSR for the role exceeds the threshold, the AMSR governs. If the threshold exceeds an unusually low market rate, the threshold governs.

The AMSR rules were updated by the Migration Legislation Amendment (Annual Market Salary Rate) Instrument 2026, commenced 25 March 2026. Where a Fair Work instrument or state industrial instrument applies, nominators can now choose between the existing instrument-based rate and an alternative methodology drawn from employment documents or external market data, provided the figure is not less than the rate under the applicable instrument. The amendment applies to nominations lodged on or after 25 March 2026 and to undecided nominations lodged earlier.

The “earnings” definition does not change with that amendment. AMSR is still calculated on base earnings, excluding compulsory super, the same way as CSIT and SSIT.

Worked example: a 186 Direct Entry nomination at the boundary

Consider a sponsor preparing a 186 Direct Entry nomination for a Software Engineer in Sydney. The role passes Skills Assessment and the candidate has the experience. The contract is in front of the founder for sign-off. There are two scenarios.

Scenario A: $76,515 total package

Contract clause: “Total annual remuneration $76,515 inclusive of 12% superannuation.”

Calculation Home Affairs will perform:

- Total package: $76,515

- Less SG component (12% of base): work the maths backward, base equals $76,515 divided by 1.12, which is $68,317

- Earnings figure for the threshold test: $68,317

Result: the nomination is below CSIT, currently $76,515. The application is refused.

This is the most common version of the mistake. The figure on the offer letter looks like the threshold figure, but the structure means the cash salary is well short. The same nomination prepared for lodgement after 1 July 2026 would be even further below the indexed CSIT of $79,423.

Scenario B: $76,515 base salary plus super

Contract clause: “Base annual salary $76,515. Superannuation paid in addition at the prevailing legislated rate.”

Calculation Home Affairs will perform:

- Base salary: $76,515

- Earnings figure for the threshold test: $76,515

Result: the nomination meets CSIT for 2025 to 2026 lodgements. The total cost to the employer is $76,515 plus 12% SG, which is $85,696.80 cash plus super for the year. The employer is now budgeting accurately, and the nomination is structurally sound.

The same role lodged on or after 1 July 2026 would need a base of at least $79,423 to clear the indexed CSIT. AMSR for a Sydney Software Engineer will likely exceed that, so the AMSR test will be the binding floor.

What counts and what does not: the line-by-line view

| Item | Counts toward earnings? | Why |

|---|---|---|

| Base salary, paid in cash | Yes | Wages under reg 2.57A and s 332 |

| Guaranteed contractual bonus, fixed amount | Yes | Determinable in advance |

| Discretionary bonus, “up to” or “may be paid” | No | Discretionary payments are excluded |

| Commission, fixed and guaranteed minimum | Partly | Only the guaranteed minimum portion |

| Commission, performance based and variable | No | Cannot be determined in advance |

| Guaranteed overtime, fixed in the contract | Yes | Contractually guaranteed |

| Overtime, ad hoc or expected | No | Not determinable in advance |

| Compulsory employer superannuation (SG) | No | Expressly excluded by reg 2.57A and s 332(4) |

| Voluntary employer super, above SG | Sometimes | Get specific advice; FW case law allows it in some cases |

| Salary-sacrificed amounts that would have been wages | Yes | Amounts applied as the employee directs |

| Non-monetary benefit, money value agreed in writing | Yes | Reasonable money value, agreed in writing |

| Non-monetary benefit, no agreed money value | No | Cannot be quantified |

| Living-Away-From-Home Allowance | Generally no | Treated as a reimbursement of expenses |

| Reimbursements (travel, expenses) | No | Reimbursements are excluded |

| Sign-on bonus, one-off | No | Not annual recurring earnings |

| Share scheme grants | Case by case | Need contract specifics |

If you would like a clean summary of who pays what across employer-sponsored visas more broadly, our 482, 494 and DAMA cost guide walks through the cost-recovery rules under reg 2.87 in detail.

A real-world pattern from migration practice

A small-business owner came to us last quarter. They had a 485 visa holder working with them as a “Program or Project Administrator”. They wanted to sponsor the worker through a Subclass 482 Core Skills nomination. The 485 visa holder was already working with the company at $80,000 inclusive of super, with a “performance bonus of up to $8,000”. The founder was confident the package was well above CSIT.

Two structural problems surfaced when we worked through the figures.

First, the cash component was $71,429. Once the SG was stripped out, the contract sat below CSIT and would have been refused on the threshold test alone, before the AMSR was even considered.

Second, the bonus was discretionary. Even if the contract had been worded as $80,000 plus super, the discretionary bonus could not have been counted toward the threshold. To make the bonus count, the wording would need to be a guaranteed minimum, paid annually, with the amount fixed in the contract.

We re-papered the role at $82,500 base, super on top, with a guaranteed annual retention payment of $4,000 paid at the 12-month anniversary. Earnings figure for the threshold test became $86,500. The contract cleared CSIT and the AMSR for the occupation, the founder’s total cost to the business was clear, and the nomination went through cleanly.

If you are at the contract-drafting stage, our visa cost estimator and visa blueprint assessment will help your finance team budget the full sponsorship cost before the offer is signed.

Where FWHIT fits in employer-sponsored migration

The Fair Work High Income Threshold sits outside the Migration Regulations, but it shows up in three places that matter for employer sponsorship.

- 186 Direct Entry age waiver. Applicants over 45 may rely on the high-income earner exemption if they have been earning at or above the FWHIT for at least the three years immediately before applying. The earnings test mirrors section 332, so the same exclusion of compulsory super applies.

- 482 age and English concessions. Certain pathways for older or longer-serving applicants reference earnings at or above the FWHIT.

- Specialist Skills stream context. The Specialist Skills stream sits at a higher tier than FWHIT, and the SSIT for 2025 to 2026 of $141,210 is sometimes referenced alongside FWHIT in policy discussions.

FWHIT is published by the Fair Work Commission and indexed annually on 1 July. The 2026 to 2027 figure is $190,100, up from $183,100 for 2025 to 2026.

Common mistakes that get nominations refused

Drawn from refusal patterns and recent migration-law commentary, these are the contract issues we see most often.

- Salary quoted as a “total package inclusive of super”. The cash component is what counts, and it is almost always lower than the package figure.

- Discretionary bonuses included as part of the threshold figure. If the wording uses “up to”, “may be paid”, “subject to performance review” or similar, the amount is not earnings.

- Variable overtime treated as guaranteed. Only fixed contractual overtime counts.

- Non-monetary benefits without an agreed money value. A car or housing allowance with no written value cannot be added.

- The SG rate change overlooked. With SG at 12% from 1 July 2025, contracts written under the older 11.5% framework can fail the cash-component test even if total package figures look unchanged.

- Reliance on AMSR data that does not match the location, occupation code or comparator profile. The 25 March 2026 AMSR amendments give nominators more flexibility on evidencing, but the figure still has to be defensible.

- Forgetting the dual test. CSIT, SSIT and AMSR are independent. The nominee must be paid the higher of the threshold and the AMSR.

If a refusal pattern keeps surfacing across your nominations, reach out to a registered migration agent and we can audit the contract template before the next role is advertised.

Pre-lodgement contract checklist

Run this against the offer letter before the nomination is lodged.

- Is the base salary stated separately from super, in dollars, in the contract?

- Is the cash component, before super, at or above the applicable CSIT or SSIT for the lodgement date?

- Does the cash component plus any guaranteed contractual amounts also clear the AMSR for the occupation in that location?

- Are bonuses described as guaranteed, with a fixed annual minimum amount, rather than discretionary?

- Is overtime fixed and contractual rather than variable or expected?

- If a non-monetary benefit is being counted, is the money value agreed in writing?

- Has any reimbursement, allowance or one-off payment been removed from the threshold figure?

- For lodgements on or after 1 July 2026, has the cash component been re-tested against the indexed CSIT of $79,423 (and, for Specialist Skills nominations, the 2026-27 SSIT once the Department publishes it)?

- For an over-45 186 DE applicant relying on FWHIT history, has the three-year earnings record been verified against section 332?

If any answer is “no” or “not sure”, the nomination needs another pass before it goes to the Department.

Get the contract right before you lodge

WiseKangaroo prepares 482, 494 and 186 nominations for Australian sponsoring employers, and we review contracts at the offer-letter stage so the structural issues above never make it into a refusal. If you have a nomination on the way and want a second set of eyes on the salary structure, book a consultation and we can walk through the figures with you.

Plenty of helpful tools live in the resource hub, including the visa cost estimator, the visa blueprint assessment, and the full visa guides library for cross-referencing eligibility against your candidate’s profile. Our explainer on the current TSMIT/CSIT figure is a useful one-page refresher to keep with the contract.

Frequently asked questions

Q: Is super included in TSMIT, CSIT or SSIT? A: No. Compulsory employer superannuation is excluded from “earnings” by reg 2.57A of the Migration Regulations 1994 and by section 332 of the Fair Work Act 2009. The figure tested against the threshold is the cash salary plus guaranteed contractual amounts, before SG is applied.

Q: Does the CSIT change on 1 July 2026? A: Yes. The CSIT (also referenced as TSMIT under reg 5.42A) rises from $76,515 to $79,423 for nomination applications lodged on or after 1 July 2026. The SSIT for 2025 to 2026 is $141,210; the indexed 2026 to 2027 figure has not been published in the same instrument and should be verified with the Department before lodging a Specialist Skills nomination.

Q: Does the AMSR test exclude super as well? A: Yes. AMSR is calculated on annual earnings under reg 2.57A, the same definition that applies to CSIT and SSIT. Compulsory super is not part of the comparator figure for an equivalent Australian worker either.

Q: My contract says “$80,000 inclusive of super”. Will that meet CSIT? A: Probably not. With SG at 12%, a package of $80,000 inclusive translates to a base salary of about $71,429 cash, which is below CSIT. A contract structured as “$80,000 base salary plus super” is the version that clears the threshold.

Q: Do guaranteed bonuses count toward the threshold? A: Only if the amount is genuinely guaranteed in writing and quantifiable in advance. A clause that says “up to $5,000” or “subject to performance” is discretionary, and Home Affairs will not include it. A clause that says “an annual retention payment of $4,000, paid on each anniversary” is generally counted.

Q: What about voluntary employer super above the SG amount? A: Voluntary employer contributions above the SG amount can count as earnings under section 332(4), and there is Fair Work Commission case law supporting that treatment. Get specific advice before relying on this for a borderline contract, because the documentation needs to be precise.

This article is for general information only. Migration law and salary thresholds change regularly, and individual circumstances vary. For specific advice about your nomination or visa, consult a registered migration agent. WiseKangaroo migration agents are MARN-registered and authorised to provide Australian immigration assistance.